GST Refund Process: Understanding the Cash Ledger

Electronic Cash Ledger: Electronic cash ledger is a cash ledger maintained in the electronic form on the GST portal. Electronic cash ledger contains details of all the deposits made by a taxpayer under GST. Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) is also reflected in electronic cash ledger of the taxpayer. […]

GSTN Enabled Functionality for LUT Submission

One such development in the realm of Goods and Services Tax (GST) is the introduction of GSTN enabled functionality for furnishing the Letter of Undertaking (LUT) for the Financial Year 2024-25. The Letter of Undertaking (LUT) plays a crucial role for exporters, allowing them to supply goods or services without paying integrated tax. Instead of […]

A Guide to Opting for the Composition Scheme for Financial Year 2024-25

As the financial year 2024-25 unfolds, taxpayers find themselves grappling with various compliance requirements, including those related to the Goods and Services Tax (GST). Among the options available to taxpayers is the Composition Scheme, a simplified taxation scheme aimed at easing the compliance burden for small businesses. In this blog post, we will delve into […]

Data Analytics and AI Technical Tools Helps DGGI Cracks Down on GST Fraud: 1,700 Cases and 98 Arrests

In a significant crackdown on tax evasion, the Directorate General of GST Intelligence (DGGI) has made substantial headway in the Financial Year 2023-24, uncovering 1,700 fraudulent Input Tax Credit (ITC) cases amounting to a staggering Rs. 18,000 crores. This concerted effort has resulted in the apprehension of 98 individuals involved in these nefarious activities, marking […]

GST Audit Notices: Understanding the Extended Time Limit for Issuing Notice and Orders under Section 73

Introduction: In the realm of GST compliance, receiving audit notices can be daunting for businesses. However, staying informed about regulatory updates can alleviate some of the uncertainties. One recent development worth noting is the extension of the time limit for issuing orders under Section 73 of the GST Act. Let’s delve into what this means […]

Navigating GST Refunds for E-Commerce Businesses: A Comprehensive Guide

Introduction: In the dynamic world of e-commerce, where transactions happen at the click of a button, understanding the nuances of Goods and Services Tax (GST) refunds is crucial for businesses to optimize their financial operations. GST refunds play a significant role in ensuring that businesses can recover the taxes they paid on inputs, thereby preventing […]

Navigating the Tax Maze: Your Ultimate Guide to GST Insights (Feb 2023 – Jan 2024)

Description: Dive into the dynamic world of Goods and Services Tax (GST) with our comprehensive blog series. From the latest regulatory updates to expert insights on compliance, our curated collection of articles covers everything you need to know about GST. Stay informed, make strategic decisions, and empower your business with the knowledge to navigate the […]

Key GST Case Laws (Feb 2023 – Jan 2024): Navigating Legal Precedents in Taxation

Explore the dynamic landscape of Goods and Services Tax (GST) through our curated compilation of the “Top 24 Case Laws” spanning from February 2023 to January 2024. This comprehensive collection delves into pivotal legal precedents, providing valuable insights into the evolving nuances of GST regulations. From landmark decisions to nuanced interpretations, these case laws offer […]

Complying with the Law: Mandatory Bank Account Details Submission for GST Registered Taxpayers

Introduction: Ensuring compliance with the Central Goods and Services Tax (CGST) Act, 2017, is paramount for businesses operating within the GST framework. One critical aspect of this compliance is the mandatory submission of bank account details by registered taxpayers. In this blog post, we will explore the legal provisions requiring this submission, the consequences of […]

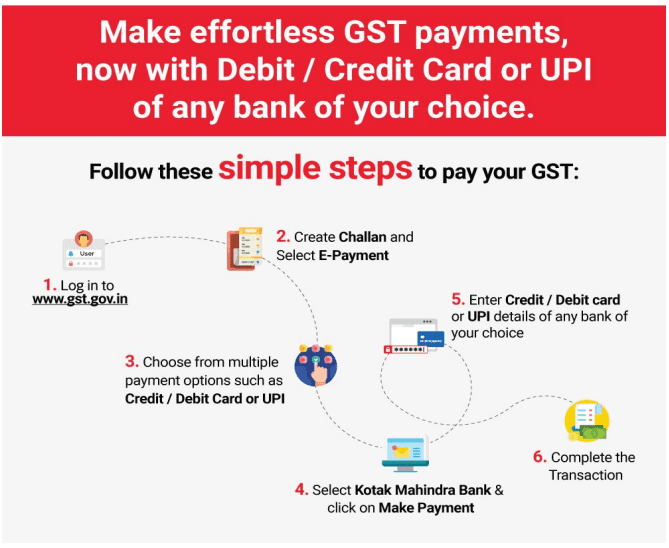

Expanding Horizons: New Payment Options for GST Taxpayers

Introduction: In a move to enhance convenience for taxpayers registered under the Goods and Services Tax (GST), the government has introduced two additional methods of payment under the e-payment system. These new facilities, namely Credit Card (CC) and Debit Card (DC), along with Unified Payments Interface (UPI), offer taxpayers more flexibility in managing their financial […]