GST on Sale of Used Vehicles is a topic that confuses many business owners and professionals.

When a business buys a vehicle and later sells it, a common question arises. Should you claim Input Tax Credit at the time of purchase or should you avoid ITC and pay GST only on margin at the time of sale.

Many people believe that paying tax on margin always saves GST. In reality, that is not always true. In many genuine business situations, claiming ITC turns out to be more beneficial than the margin scheme.

This blog explains this in a simple and practical way so that you can decide what suits your case best.

The Two Cases in GST

Case 1: Claim ITC at Purchase:

- You take credit of GST paid

- You use it against your GST liability

- On sale, GST applies on full value

- ITC gets reduced by 5 percent per quarter till sale as per Rule 40

Case 2: Do Not Claim ITC and Use Margin Scheme:

- You do not take GST credit at purchase

- You pay GST only on margin under Rule 32

- Margin depends on buyer type:-

| Buyer Type | Margin Formula |

| Unregistered | Sale Value – Purchase Cost |

| Registered | Sale Value – WDV at sale |

Let’s understand with An Example

Let us take a simple, realistic business case.

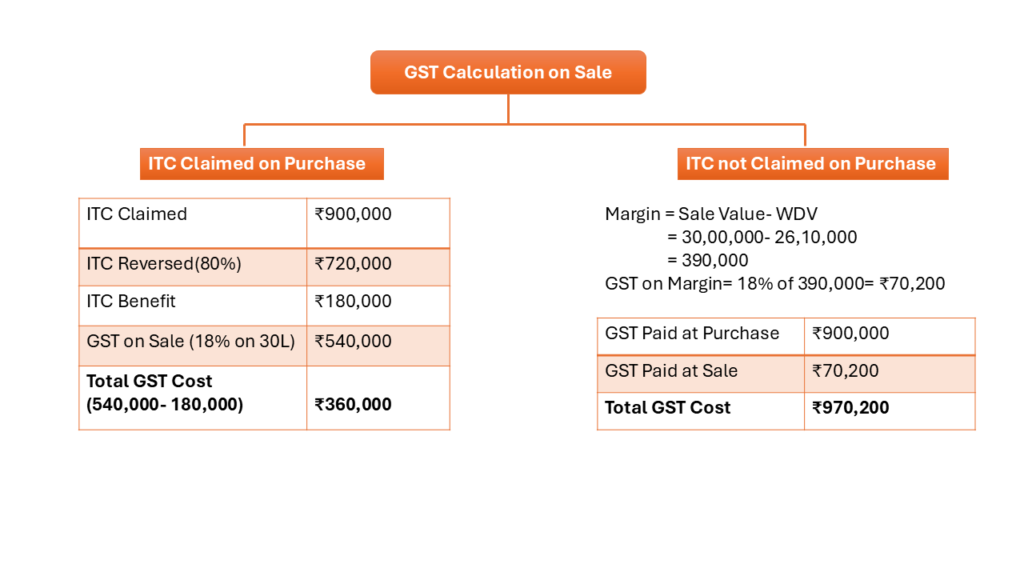

| Particulars | Amount |

| Purchase Value | ₹50,00,000 |

| GST Rate | 18% |

| Sale Value | ₹30,00,000 |

| Sold After | 4 years |

| Buyer | Registered |

ITC Reversal Rule: 5% per quarter (Rule 40 CGST)

Number of quarters in 4 years = 16

ITC reversal = 16* 5% = 80%

WDV of vehicle after 4 years = ₹26,10,031

Even after reversing 80% ITC due to early sale, the ITC route still saves more than ₹6 lakh.

What This Comparison Clearly Shows

- Paying GST only on margin looks cheaper at sale stage

- But it ignores GST already absorbed at purchase

- ITC, even after reduction, continues to give a net advantage

- The tax burden should be evaluated across the entire life of the asset, not only at the time of sale

Does Margin Scheme Ever Overtake ITC

Margin scheme becomes relevant mainly when:

- ITC is blocked under Section 17(5)

- Vehicle is used for personal or employee purposes

- Business deals in used vehicle trading Market pricing does not allow full GST pass through

- Sale Value is more than Purchase value (which is not possible in practical scenario).

Final Thoughts

GST on Sale of Used Vehicles is not about choosing the cheaper option at the time of sale. It is about choosing the smarter option at the time of purchase.

When ITC is legally available and usable, claiming ITC almost always results in a lower overall GST burden than relying on the margin scheme, even after applying the 5 percent per quarter ITC reduction.

Margin scheme is a compliance mechanism, not a tax saving shortcut.

A business that plans GST on vehicles at the purchase stage saves significantly more than one that reacts only at the time of sale.

LinkedIn Link : RMPS Profile

Prepare by : Aditi Soni www.linkedin.com/in/aditi-soni-368113317

This article is only a knowledge-sharing initiative and is based on the Relevant Provisions as applicable and as per the information existing at the time of the preparation. In no event, RMPS & Co. or the Author or any other persons be liable for any direct and indirect result from this Article or any inadvertent omission of the provisions, update, etc if any.

Published on: January 28, 2026