Change Authorised Person in GST Portal is an important compliance activity that every GST-registered business must handle carefully. Authorised person details play a critical role in GST compliance, and any mismatch, inactive signatory, or outdated information can result in return filing failure, inability to generate e-invoices, missed notices, or even penalties. This advanced guide explains not only the step-by-step procedure but also covers legal provisions, practical scenarios, portal-level differences, compliance risks, FAQs, and professional best practices in a simple and structured manner.

Who Is an Authorised Person / Authorised Signatory?

An authorised person is an individual officially empowered by the taxpayer to act on their behalf. In simple terms, this person is legally allowed to perform compliance-related activities under GST. Primarily, the authorised signatory operates on:

- The GST Portal

- Related GST systems, such as refunds, appeals, notices, and replies

Therefore, any action taken by the authorised person is treated as an action of the taxpayer itself.

Legal Reference

- Section 26 of CGST Act, 2017 – Actions taken by an authorized signatory are deemed to be actions of the taxpayer.

This means any mistake by the authorized person directly impacts the taxpayer.

When Is Authorised Person Change Mandatory?

Authorised person change becomes mandatory in cases such as:

- Change in director / partner / proprietor

- Resignation or termination of employee or consultant

- Change of CA, accountant, or GST practitioner

- Death or incapacity of authorized person

- Security reasons (data misuse risk)

Consequently, delay in updating may result in compliance disruption and potential legal exposure.

Documents & Information Required (Advanced Checklist)

- PAN of new authorized person

- Aadhaar (for authentication)

- Active mobile number & email ID

- Authorization letter / board resolution / partnership consent

- DSC (mandatory for companies & LLPs)

Detailed Process: Change Authorised Person in GST Portal

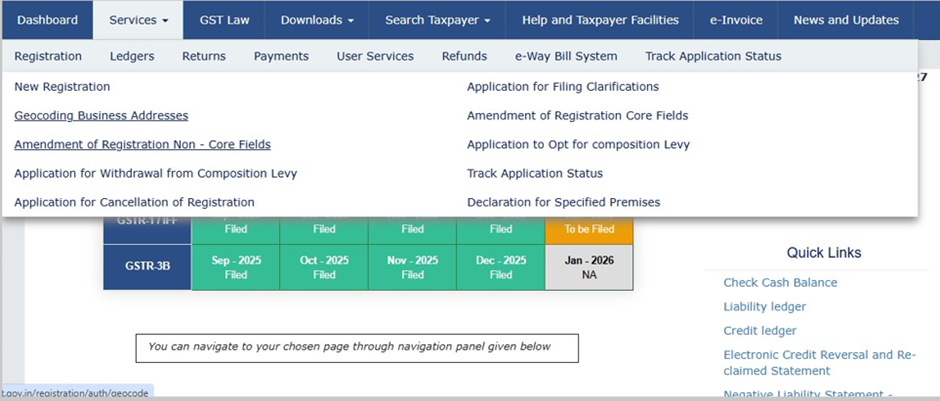

Login to GST Portal

Access www.gst.gov.in using existing authorised credentials.

Amendment of Registration

Path: Services → Registration → Amendment of Registration (Non-Core Fields)

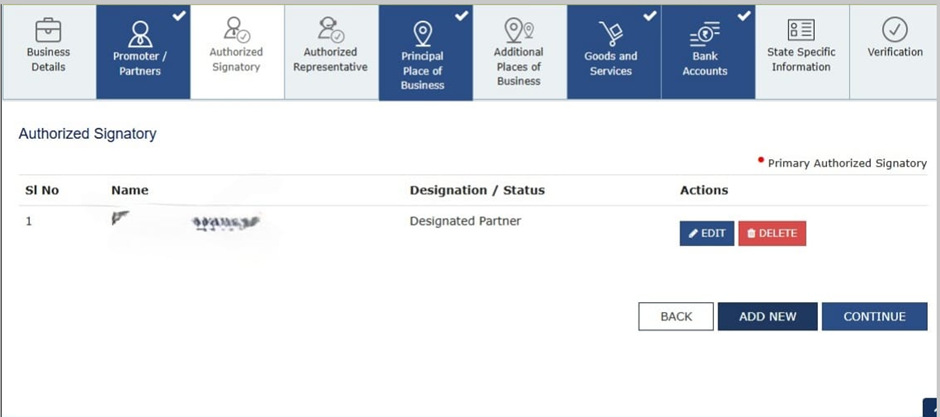

Authorised Signatory Tab

- Open the Authorised Signatory section

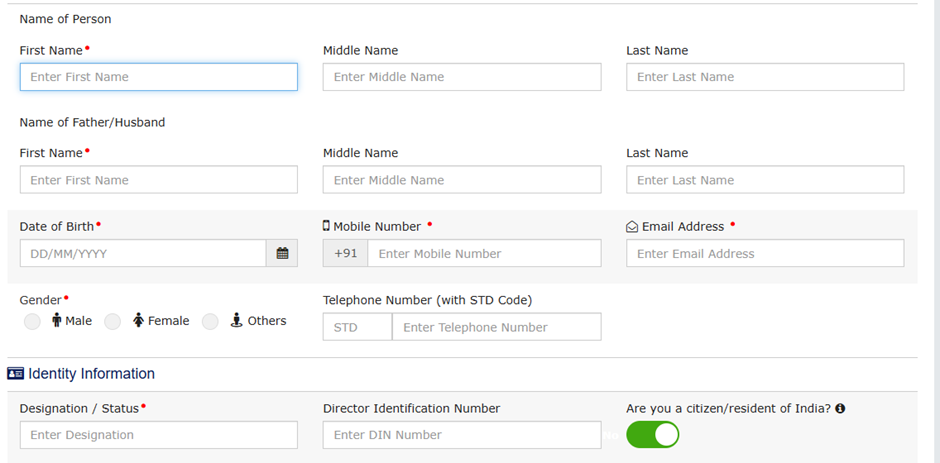

Add New Authorized Person

- Click Add New

- Enter PAN-based details

- Choose role: Primary / Secondary

- Primary authorised person has full control including adding/removing others.

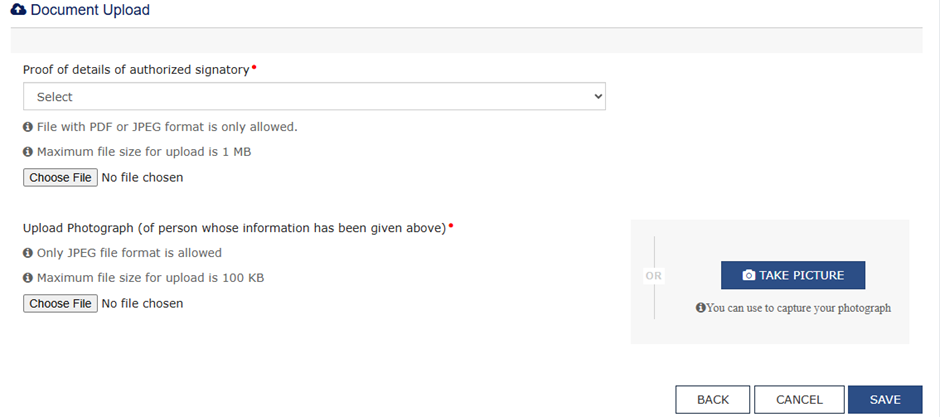

- Upload Document

- Then after Save this with otp

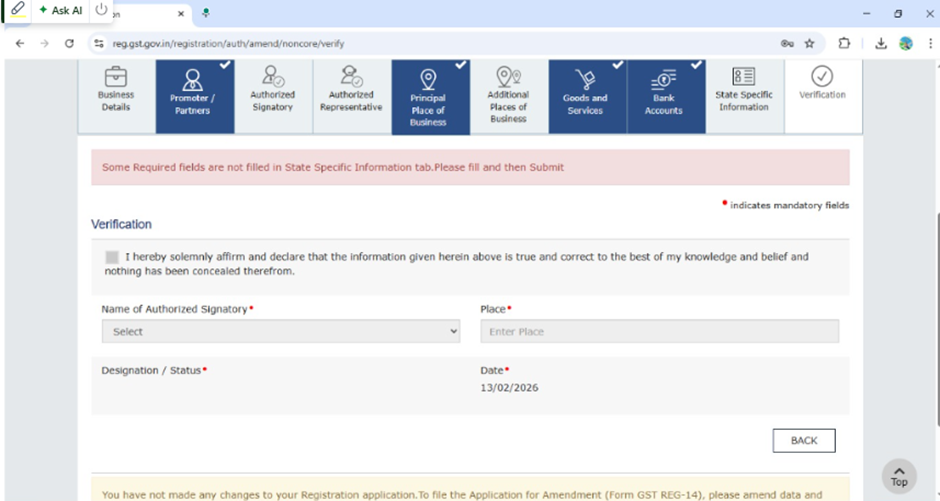

Verification & Submission

- Submit using DSC / EVC

- No officer approval required

- Amendment effective immediately

Common Practical Issues & Solutions

1. Aadhaar Authentication Failed

✔If the issue persists, retry the authentication process after 24 hours.

2. PAN Name Mismatch

✔ Before proceeding, verify that the spelling is exactly the same as recorded in the PAN database.

3. OTP Not Received

✔First, check the spam or junk folder in your email inbox.

4. E-Invoice Access Not Working

✔ Confirm separate user creation on e-invoice portal

Compliance Risks If Not Updated

Consequently, failure to update the authorised person can result in:

- Inability to file GSTR-1 / GSTR-3B

- Blocked e-invoice generation

- Missed GST notices & deadlines

- Penalty exposure due to non-compliance

- Risk of data misuse by ex-employees

Best Practices (Professional Tips)

- Firstly, review authorised persons on a quarterly basis to ensure details remain accurate and updated.

- Secondly, limit primary signatory rights to maintain better internal control and reduce risk exposure.

- Additionally, maintain proper authorization documents and resolutions on record for audit purposes.

- Furthermore, deactivate user access immediately when an employee or consultant exits the organization.

- Finally, test e-invoice portal access after every authorised person change to avoid operational disruption.

Conclusion: –

Therefore, authorised person change in GST portal is not just a procedural task — it is a critical compliance control. Moreover, timely updating safeguards the business from operational disruption, legal risk, and data misuse.Following a structured and documented approach ensures smooth GST compliance.

LinkedIn Link : RMPS Profile

Prepared by : Jaya Vadhwani

This article is only a knowledge-sharing initiative and is based on the Relevant Provisions as applicable and as per the information existing at the time of the preparation. In no event, RMPS & Co. or the Author or any other persons be liable for any direct and indirect result from this Article or any inadvertent omission of the provisions, update, etc if any.

Published on: February 17, 2026