What is Job-Work Under GST?

The definition of Job-work under GST is covered under section 2(68) of the CGST Act, 2017 states “Any treatment or process undertaken by a person on goods belonging to another registered person”. Therefore, a job worker is a person (registered or unregistered) who is processing or treating the goods of another registered person and the owner of the goods is called the Principal in this respect. Section 19 of the CGST Act, 2017 explains the definition of the Principal as ‘a person supplying goods to the job-worker.’

Job Work GST Rate

The rate of GST on job work is as follows.

- The GST council has decreased the tax rate on engineering work from 18% to 12%

- Diamond supply work is subject to a 1.5% GST Rate down by 5%

Also, in the most updated GST circular of 2019, it was clearly stated that all enrolled taxpayers under job work would be charged 12% GST, while unregistered taxpayers would be charged 18% GST.

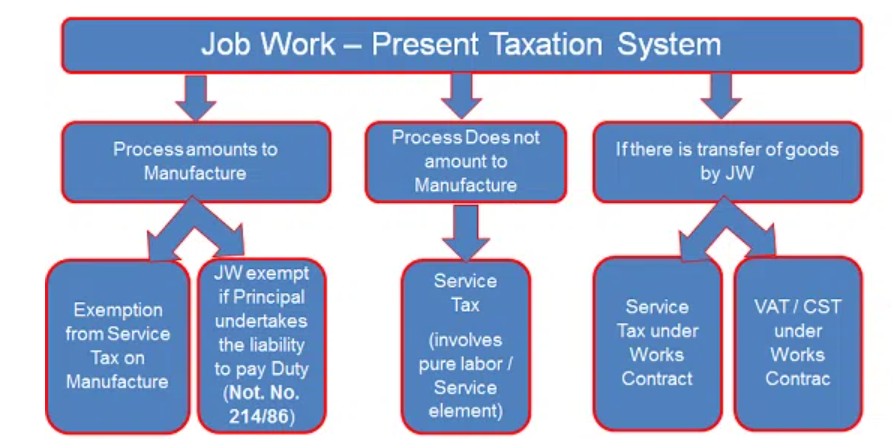

Moreover, one initially needs to know their job work under GST. In general, GST valuation would be the transaction value, and such cost would be considered the sole consideration for GST purposes. Although in practice, many expenses are borne on the behest of the job worker by the main.

Input Tax Credit (ITC) on goods sent for Job Work

- Goods can be sent to job worker from the Principal place of business or directly from the place of supply of the supplier of such goods.

- The Principal is entitled to take input tax credit on inputs and capital goods sent for job work even if the inputs are directly sent to job worker.

- If the goods sent on job work are not received back within the respective time limits, it shall be deemed supply from the principal to job worker on the date of goods sent or receipt of goods at job worker premises.

Time Limit for receipt of goods from Job Worker to Principal

The goods sent by the Principal must be received by him in the following time limit.

Input Goods: The input goods should be received within 1 year.

Capital Goods: The Capital goods should be received within 3 years

- If the goods are sent from Principal Place of Business, the time limit of 1 year / 3 years should be from the date of goods sent.

- If the goods directly sent from place of supply of supplier of such goods: 1 year / 3 years should be from the date of receipt of said inputs at the job worker’s premises.

Form ITC 04

Form ITC 04 contains details of inputs and capital goods sent to and received from a job worker. This form needs to be filed by every principal manufacturer who is sending goods for job work on quarterly basis.

This Article is only a knowledge-sharing initiative and is based on the Relevant Provisions as applicable and as per the information existing at the time of the preparation. In no event RMPS & Co. or the Author or any other persons be liable for any direct and indirect result from this Article or any inadvertent omission of the provisions, update etc. if any.

Published on: September 18, 2023